Federal Construction Administration Finance on the County away from Utah

The newest Government Housing Management, are not known on the phrase off FHA, try oriented 82 years back. It had been to start with introduced about aftermath of the financial demands presented of the High Despair. Which authorities team suits to help Us americans inside their pursuit of home ownership.

The brand new FHA will bring very competitive real estate loan desire financing costs together that have greatest-level refinance selection. These types of choices are around for folks who are into hunt for home financing insured by FHA together with men and women who do maybe not appeal instance insurance policies. As of 2016, this new FHA ‘s the world’s premier financial insurance carrier.

The basics of the new FHA’s Repaired Rate Mortgage loans

A fixed price mortgage is sometimes available to anyone who has below stellar borrowing. Certain people only use up all your a credit history but really are designed for showing on the bank they’ve a reputation for expenses costs generated with the-some time when you look at the-full. The FHA utilizes what is described as good sense underwriting. For the layman’s terms and conditions, sound judgment underwriting function brand new FHA will not only take a look at a possible borrower’s credit history. Alternatively, brand new FHA examines many other variables like the candidate’s big date hands on, whether his paycheck might have been uniform over the past ages and you can whether or not he has got repaid his book regularly. Anyone who has a credit score from 580 or even more is eligible for the fresh new FHA’s fixed rate financial. This form of financial is also offered to people that can also be simply manage to shell out step 3.5 per cent (or more) of one’s house’s total cost in the form of a lower fee. There are not any pre-fee penalties. The fresh repaired price home loan exists that have a great 15, 20, 25 otherwise 29-year term.

Have the Golf ball Rolling on the FHA Home loan by making use of Now

The FHA mortgage application is on our site. You are able to complete supporting records and look your application’s reputation toward all of our web site. If you have questions or questions, take a moment to arrive out to our mortgage experts having guidelines.

FHA Home loan Standards

If you do not has a great credit score, many years of steady earnings or any other typical official certification to possess property financing, you will still might qualify for an excellent FHA mortgage. Even if FHA loan wide variety disagree because of the part and you can possessions type of, he’s nevertheless among safest home loans locate. Let me reveal exactly what just be sure to be eligible for good FHA Home loan:

- A FHA financial applicant’s advance payment number determines the particular level away from credit history considered appropriate. Including, home financing applicant having a credit rating throughout the variety regarding five-hundred and 579 are needed so you’re able to plunk off an very first advance payment one equates to at least 10 % out-of the latest residence’s worth. A home loan applicant who does choose build a straight down payment on general variety of step 3.5 % so you can nine % will be required for a good minimum credit score out-of 580 or maybe more.

- FHA home loan individuals must confirm he has an uninterrupted records regarding a position. It is possible so you can be eligible for so it kind of home mortgage if an individual has worked getting just one company throughout the a couple of successive decades preceding the FHA mortgage application distribution.

- The latest candidate need to confirm one his societal cover matter are genuine, that he’s off their country’s court decades to get a home loan and that the guy legally lives in the us.

- New borrower’s deposit should be no less than step 3.5 % of your own home’s sales price. If the prospective buyer do not want such as a deposit, he can nevertheless be accepted to have a beneficial FHA mortgage if the money is actually gifted in order to your of the a member of family.

- An effective FHA financial applicant might also be expected to pay a couple of type of style of home loan insurance money. The foremost is paid back at once at the beginning of new residence’s acquisition. Alternatively, you https://paydayloancolorado.net/cathedral/ can fund this mortgage insurance premium into the borrowed funds. The next mortgage advanced are paid down monthly.

- Merely top home occupancy land meet the requirements for sale toward the means to access an effective FHA loan.

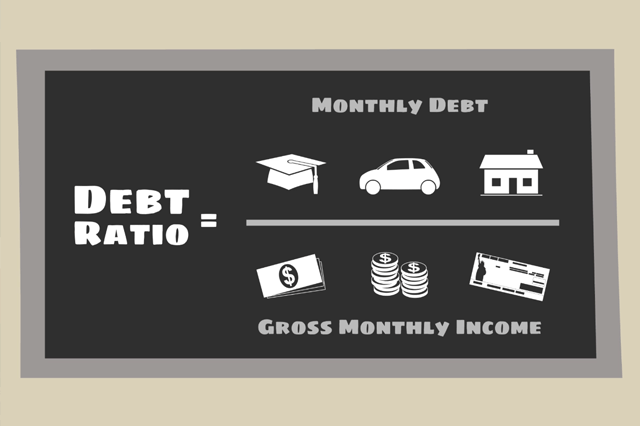

- The latest debtor need to have a top-stop proportion out of 31 per cent or less of their revenues. Leading-prevent ratio is actually determined with the addition of the loan payment on cost of homeowners’ insurance, the cost of home loan insurance rates and you will HOA charge. Though it is achievable to acquire acceptance that have a side-stop proportion upwards of 40 percent, acceptance tend to hinge toward lender’s capacity to confirm you to definitely stretching the mortgage provide is a risk value delivering.

- The fresh borrower’s back-prevent ratio must be 43% regarding their revenues otherwise quicker. The trunk-end ratio are determined adding the newest borrower’s mortgage in order to his month-to-month bills including his auto note, the price of their student education loans, credit card money and you will past.

- In case the debtor features stated case of bankruptcy, the guy have to be a couple of years removed from that it statement. Such as one must possess re also-mainly based their borrowing. Conditions to that particular standard try it is possible to if your applicant could have been taken off bankruptcy for longer than annually. For the most part, like an exemption are granted should your bankruptcy try because of extenuating things not in the mortgage applicant’s manage.